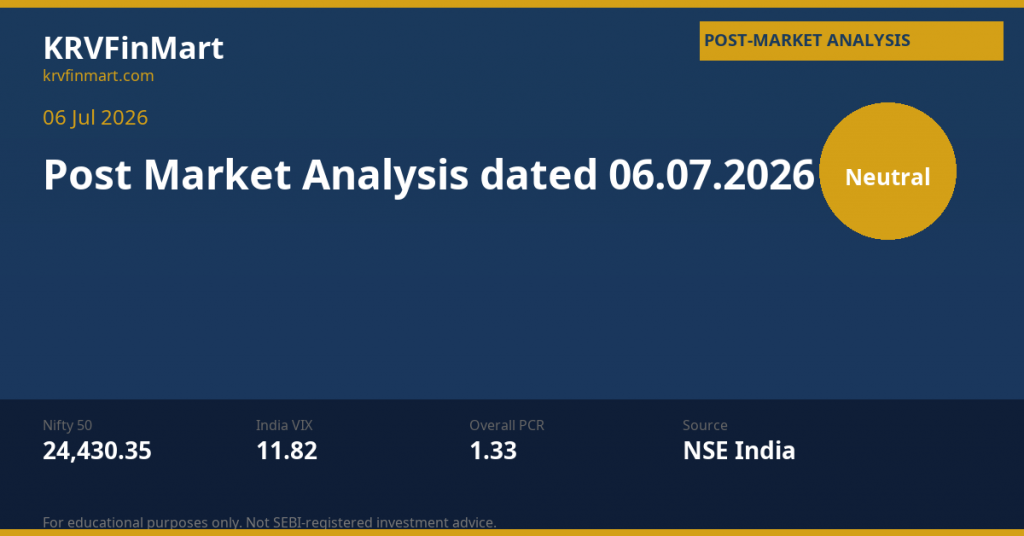

Post Market Analysis (Outlook for: 01.07.26)

KRVFinMart — Daily Market Outlook

Key Market Signals — Data: 01 Jul 2026

|

Overall PCR

1.11

▲ +0.00%

PCR at 1.11 — puts exceed calls in OI, signalling a mild bullish undertone with modest downside hedging in place

|

India VIX

13.24

▲ +0.00%

VIX flat at 13.24 — deep complacency zone; low fear suppresses premium but raises tail-risk of a sudden spike

|

Total OI Change

37,906,066

▼ +0.00%

Zero OI change — market-wide positions are completely static, consistent with a holiday or data-roll artefact

|

|

Futures OI

792,598

▲ +0.00%

Futures OI unchanged — no fresh directional bets were added or removed in index futures today

|

Call OI Change

6,656,859

▼ +0.00%

Call OI flat — no fresh writing or buying on the Call side; strike-level supply walls remain where they were

|

Put OI Change

7,406,260

▲ +0.00%

Put OI flat — existing put cushion (support) holds but no incremental hedging demand emerged today

|

Participant-wise Key Points

FII Structurally Bearish — Static

- Futures net: -260,059 contracts (longs 32,476 vs shorts 292,535) — FIIs remain deeply net short in index futures, a structural bearish overhang that has not budged today. The [Long Flat – Low Vol] and [Short Flat – Low Vol] tags confirm zero fresh activity; this is a carried position, not a new bet.

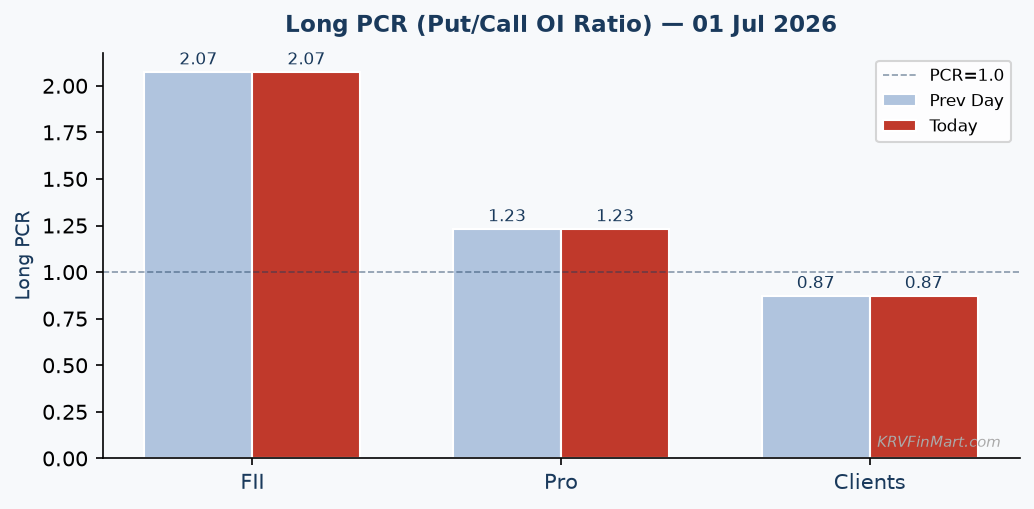

- Long PCR: 2.07 vs Short PCR: 0.56 — FIIs hold more than twice as many put longs as call longs, and far fewer put shorts than call shorts. This extreme long-put skew signals genuine bearish hedging intent, not routine premium collection. They are protecting against downside even as VIX stays low.

- Call net: -249,120 (short calls dominate) + Put net: +505,784 (long puts dominate) — FIIs are running a classic bearish combo: selling call rallies and buying protective puts. The [Long Flat / Short Flat – Low Vol] tags across all option legs indicate no conviction shift today — the bear thesis is parked, not abandoned.

- With all positions unchanged and low volume tags across the board, FIIs are in a wait-and-watch mode — likely watching for a macro trigger (global cues, RBI data, or expiry dynamics) before adding or trimming.

⟶ Tomorrow: Expect FIIs to remain net short in futures unless a strong positive catalyst forces short-covering. Their massive -260,059 net futures short creates a natural ceiling on any rally — watch for short-covering if Nifty closes decisively above 23,865 (today’s close). A rise in VIX above 14.5 alongside fresh FII put buying would confirm distribution; flat VIX with futures short reduction would signal tentative unwinding.

Pro Mildly Bullish — Static

- Futures net: +11,647 contracts (longs 40,082 vs shorts 28,435) — Proprietary desks are net long in index futures, a mild bullish stance. The [Long Flat – Low Vol] tag confirms this is a held position with no fresh conviction addition today.

- Long PCR: 1.23 vs Short PCR: 1.18 — Pros hold slightly more put longs than call longs, and slightly more put shorts than call shorts. The near-parity between Long and Short PCR suggests a balanced, delta-neutral options book — they are writing both sides selectively, typical of volatility-selling desks at low-VIX environments like 13.24.

- Call net: +110,620 (net long calls) + Put net: +166,489 (net long puts) — Pros are net buyers of both calls and puts. This is consistent with a long-straddle or long-strangle bias, positioning for a breakout move from the current range. With VIX this low, buying volatility cheaply makes strategic sense.

- All confirmation tags show [Flat – Low Vol] — no intraday activity, meaning these are purely rolled-over positions from prior sessions.

⟶ Tomorrow: Pro desks are positioned for a volatility expansion rather than a pure directional bet. If the market breaks out of today’s range (Nifty 23,829–24,036), Pros stand to benefit. Their net long futures position adds a slight bullish tilt — watch whether they add to futures longs if Nifty holds above 23,865. A range-bound day would gradually erode their long-options book via theta decay.

Clients (Retail) Cautiously Bearish — Static

- Futures net: +187,523 contracts (longs 251,066 vs shorts 63,543) — Retail clients are the largest net-long player in futures today, a contrarian warning signal. Historically, retail being heavily long while FIIs are heavily short sets up a squeeze scenario in either direction.

- Long PCR: 0.87 (more call longs than put longs) vs Short PCR: 1.28 (more put shorts than call shorts) — Retail is net bullish on calls but writing more puts than calls. The put short PCR of 1.28 indicates aggressive naked put writing — a strategy that generates income in calm markets (VIX 13.24) but carries large risk if VIX spikes.

- Put net: -697,767 — Retail’s massive net short-put position is the single largest options exposure in today’s data. This is a bullish-income strategy that implicitly bets the market won’t fall sharply. Combined with the [Long Flat / Short Flat – Low Vol] tags, this is a static, high-risk overhang going into tomorrow.

- Call net: +135,014 — Retail holds more call longs than shorts, adding to their net bullish options bias. However, being long calls at low VIX means premium paid is cheap but so is any premium collected from short puts — the risk-reward is asymmetric to the downside.

⟶ Tomorrow: Retail’s combination of net long futures (+187,523) and massive short puts (-697,767 net) makes them vulnerable to any sharp downside surprise. If Nifty breaks below today’s low of 23,829, expect forced put-short covering from retail that could accelerate selling. A stable or rising market, however, rewards their current book — watch whether they reduce put shorts near expiry as time decay benefits them.

DII Mildly Bullish — Minimal Derivatives Activity

- Futures net: +60,889 contracts (longs 72,675 vs shorts 11,786) — DIIs maintain a meaningful net long futures position, consistent with their institutional cash-market buying mandate being partially hedged. This is the strongest directional signal from DIIs.

- Options activity is minimal — DII call longs of 3,485 and put longs of 25,675 are negligible relative to other participants. No PCR ratio is calculable for DIIs as their short-side options data is effectively zero (call shorts: 0, put shorts: 179). This is typical — DIIs primarily use futures for hedging, not options for speculation.

- Put net: +25,496 — The small net long-put position suggests modest tail-risk hedging against their equity portfolio, not a directional bet. The [Long Flat – Avg Vol] tag on call longs (the only non-low-vol tag today) is a minor statistical note given the tiny absolute size of 3,485 contracts.

- All DII positions are flat with zero change today — consistent with the broader market-wide data freeze seen across all participants on 01 Jul 2026.

⟶ Tomorrow: DIIs are unlikely to drive derivatives markets tomorrow given their minimal options exposure. Their +60,889 net long futures position provides a quiet bullish underpinning. Watch the cash market for DII buying activity in Nifty/BankNifty basket stocks — that is where their real influence manifests. A sustained cash market buying program by DIIs would reinforce the mild bullish bias from PCR and pro positioning.

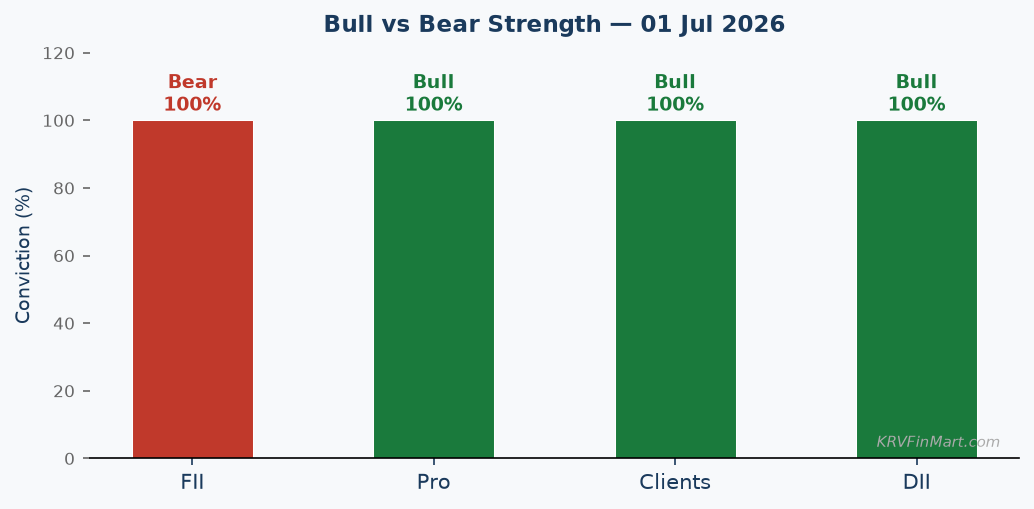

Bull vs Bear Strength

by Participant

|

FII

Structurally Bearish 78%

▼▼

|

Clients

Cautious Bull / Put Short Risk 45%

▲▼

|

Pro

Mild Bull / Vol Play 55%

▲

|

DII

Mild Bullish 60%

▲

|

Conclusion

— Market Outlook for Tomorrow (02 Jul 2026)

Today’s data presents a fully static market snapshot — every participant, every position, every OI number is unchanged at +0.00% across the board. This is a structural data signal, likely reflecting a pre-holiday, settlement, or data-roll session where no fresh positions were initiated. The underlying positioning, however, tells a clear story: FIIs are deeply net short (-260,059 futures contracts) and hold a bearish options combo (short calls, long puts), while retail clients are the mirror image — net long futures (+187,523) with a dangerously large short-put book. This classic institutional-vs-retail standoff is the dominant market structure heading into tomorrow.

VIX at 13.24 — unchanged and deeply low — confirms extreme market complacency. Historically, sustained VIX below 13.5 precedes sharp re-pricing events. With Overall PCR at 1.11 (mild put accumulation, a slight bullish tilt), the options market is not pricing fear. The Nifty/BankNifty ratio of 2.42 signals that BankNifty is outperforming Nifty — banking is the sector to watch for directional leadership. Nifty closed at 23,865.75 (range: 23,829.20 – 24,035.55) and BankNifty at 57,542.90 (range: 57,456.65 – 58,011.95). OI patterns point to a range day tomorrow, but with FII short overhang and retail short-put exposure creating a binary risk profile.

The scenario that changes everything is a VIX spike above 14.5–15.00. That level would trigger retail short-put panic covering, which could cascade into a sharp leg down — directly feeding into FII’s existing net short book. Conversely, if Nifty holds above 24,035 (today’s high) with volume, FII short-covering becomes the upside fuel. Until one of these triggers fires, the market is in a wait-and-hold mode, and tomorrow is most likely a range-bound session with elevated breakout risk in either direction.

Scenario 1 — Bull case:

Nifty sustains above 24,035.55 (today’s high) with BankNifty holding above 58,011.95. FII futures short-covering kicks in (watch for FII net futures position moving above -250,000), VIX stays below 13.00, and retail long-futures holders gain confidence. Pro long-straddle books profit on the call side. Target: upper range extension driven by short-squeeze momentum.

Scenario 2 — Bear case:

Nifty breaks below 23,829.20 (today’s low) — retail’s short-put book comes under pressure, triggering forced covering that accelerates the fall. FII net short futures (-260,059) profits on the decline. Watch for VIX crossing 14.50 as the confirmation signal of fear re-entering the market. BankNifty breaking below 57,456.65 would be the early warning — if banks crack, the broader market follows.

|

Key Resistance

24,035.55 (Nifty today’s high) — FII net short call position (-249,120 net) creates supply at and above this level; a close above it would force call-short unwinding and accelerate upside

|

Key Support

23,829.20 (Nifty today’s low) — Retail’s massive short-put book (+697,767 net contracts) provides a floor here as put writers defend their positions; break below triggers their stop-losses

|

Trigger to Watch

India VIX crossing 14.50 — at this level, retail short-put positions shift from profitable to at-risk, FII bearish positioning gains momentum, and the probability of the bear scenario rises sharply. Monitor VIX in the first 30 minutes of trade as the session’s directional cue.

|

The content provided on KRVFinMart is intended for educational and informational purposes only. We are not licensed financial advisors. ( Contact us @ https://krvfinmart.com/contact-us/ )

© KRVFinMart | krvfinmart.com

Responses